Millions of dollars for iPads – many of which ended up in a warehouse.

Then there was that thing with ClassWallet.

And we are still trying to get over the whole iStation contract debacle.

Don’t forget the million dollar price tag to “audit” DPI to determine how many more cuts should be made in the department. (The findings? DPI was underfunded.)

And then there were all those glossy flyers, emails using large databases, a construction of a personal website to conduct “superintendent” duties, and that elongated law suit against the state board that used taxpayer money to litigate.

So how fitting that this week Mark Johnson tries to score some sort of egotistical political points with this:

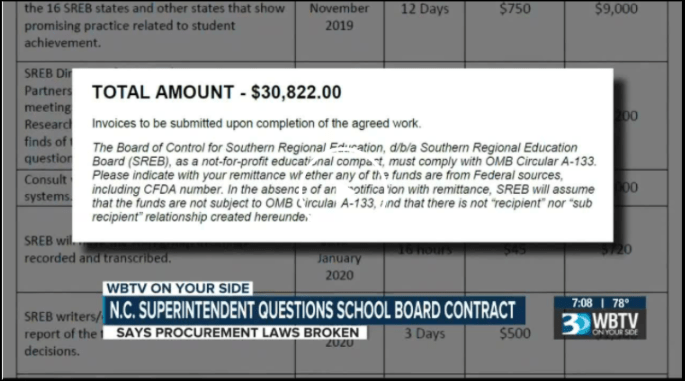

Here’s the entire complaint sent by Johnson to Beth Wood, the state auditor.

It’s about almost $31,000 dollars.

Compared the millions of dollars in questionable expenses by Johnson over his term.

But it’s rather interesting that Johnson call on Beth Wood to investigate the state board chairman for an expense when Johnson received this particular report about his own “spending habits” for just this fiscal year.

From Beth Wood.

And it talks about mishandling much more than $31,000.

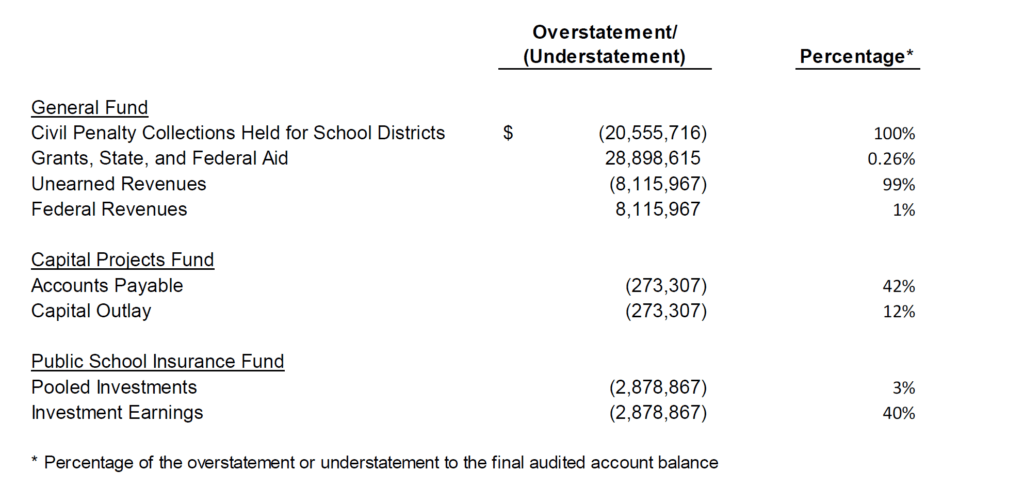

From that report:

A. The Department did not recognize the financial reporting implications of a major hurricane on the Public School Insurance Fund’s (PSIF) financial statements. Specifically, the Department:

- Did not report a $7.1 million accounting estimate for hurricane-related claims expected from insured entities, but not formally filed, until prompted by the audit.

- Did not report amounts recoverable for paid and unpaid hurricane-related claims of $5.3 million and $32.1 million, respectively.

B. The Department’s year-end accruals were not prepared or not prepared correctly. Specifically, the Department:

- Did not recognize a liability for civil penalty and forfeiture funds3 being held for school districts.

- Failed to recognize a liability for federal revenues that were unearned because they were requested and received in advance of the related disbursement.

- Incorrectly calculated and recorded the change in fair market value for pooled investments.

- Did not record payables for goods and services received but unpaid during the year.

C. The Department made other significant errors in the process of compiling financial statements, note disclosures, and required supplementary information, including:

- The fiscal year 2019 Statement of Cash Flows (Exhibit B-3) presented fiscal year 2018 amounts and did not reflect other corrections made as a result of the audit. Cash Flow Statement errors ranged from $1.9 million to $22.8 million.

- Budgetary Comparison Schedule transposed Original Budget and Final Budget amounts as defined by the Governmental Accounting Standards Board (GASB)4 and did not agree to the underlying accounting records. The most significant errors ranged from $123.8 million to $695.4 million.

Alex Granados of EdNC.org talked with Wood this week about the audit and its findings. A transcript of that can be found here.